ECONOMIC MARKET ANALYSIS: An Outlook With Risk

Content was pulled from MHI Solutions Magazine Q4.2019

Economic risks were high going into 2019. And the outlook for 2020 presents further risks.

On the upside, monetary-policy hawkishness has vanished, and the U.S. economy is in a better place than many other economies. But global economic risks abound even though U.S.-Chinese trade relations have cooled off significantly from their tensest levels in the second half of 2018. And the tensions between the U.S. and China may remain a part of the geopolitical landscape for a long time to come.

In general, economic and financial-market uncertainty is elevated, which has contributed to volatility during 2019—and could continue to do so in 2020. Plus, business investment is at risk of faded tailwinds from the fiscal stimulus and tax reform of 2017. Looking ahead to 2020, the political dynamics ahead of the U.S. presidential election are likely to be unpleasant and could spook investors. Business investment decisions in 2020 are likely to be influenced by the economic plans of the Democratic nominee as well as those of President Trump.

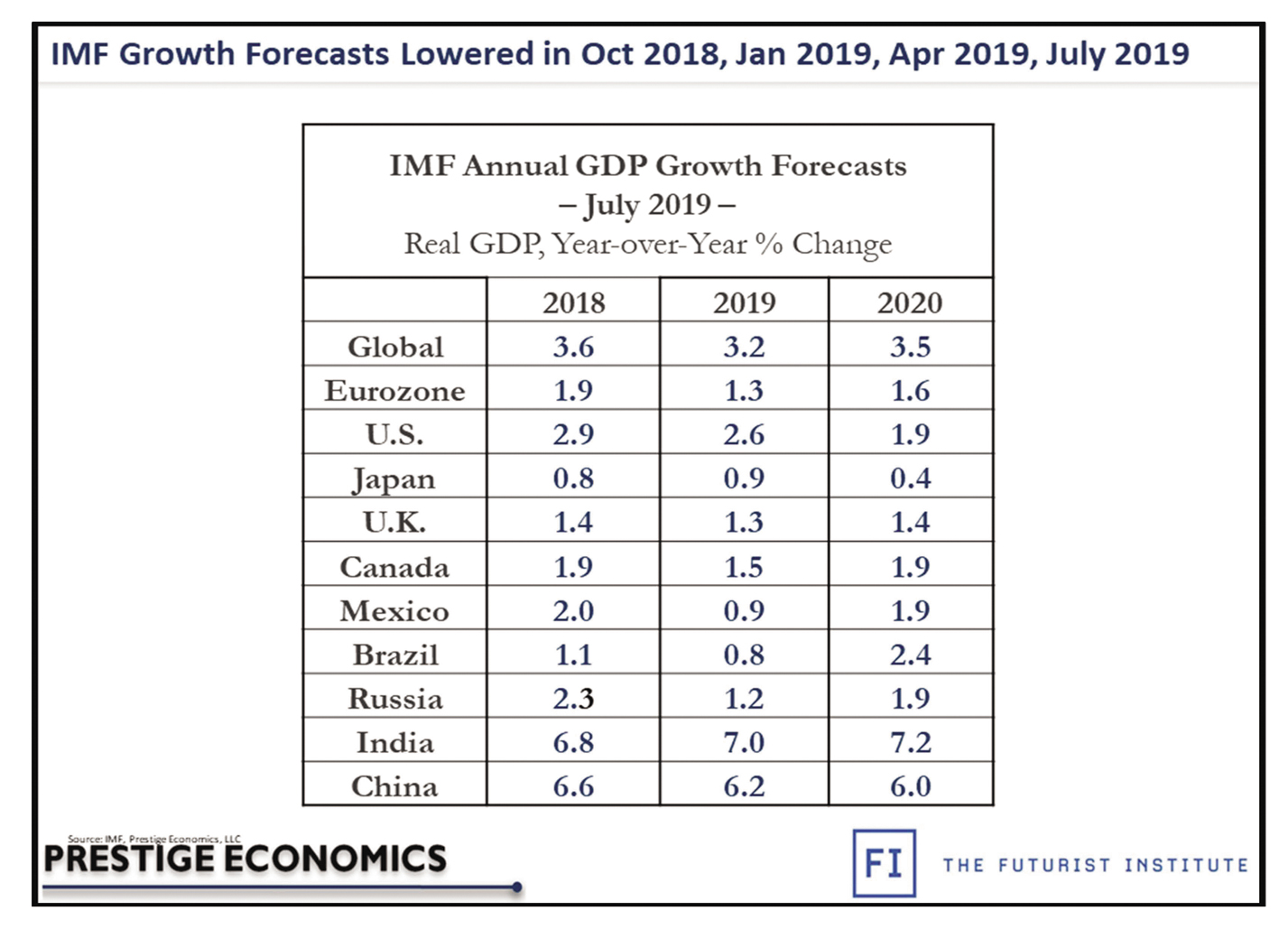

The outlook for global growth has darkened significantly in the past year. In July 2018, the IMF’s global GDP growth rate forecasts for 2019 and 2020 were still at 3.9%. At the time, the IMF warned about the downside risks to growth from trade conflicts, but the IMF was slow to actually revise its growth forecasts. Just 12 months later—in July 2019—the IMF lowered its 2019 global GDP growth forecasts in its quarterly World Economic Outlook for a fourth consecutive time to 3.2%. And the 2020 growth outlook was also lowered in July 2019 to 3.5%.

Those are much slower growth rates—but still modestly positive, even though additional downside risks remain in play.

As we look across the global economy, the downside risks to growth are greater abroad than in the U.S. This has supported a move globally toward increasingly accommodative monetary policies, including a potential resumption of quantitative-easing programs, which could bolster global growth.

On the downside, more accommodation abroad could continue to support the dollar—making foreign imports relatively cheaper and weighing on U.S. material-handling exports. This is a risk even if the Fed continues to provide further dovish forward guidance or if the Fed implements more dovish monetary policy. After all, if the U.S. is still in a better economic position than the Eurozone, China and emerging markets, the dollar could very well remain at high levels.